RETIREMENT INCOME CENTRE

Retirement Income to Last a Lifetime

Portfolio Construction With a Paycheque Portfolio™ Approach

Retirement doesn’t have to be an inevitable depletion of assets. The key is having a strategy that lets advisors deliver the retirement income clients need, without having to sell the investments that are producing the cash flow – especially when markets are down.

This distribution strategy, which Dynamic calls the Paycheque Portfolio™ approach, has one central focus: to deliver consistent income in bull and bear markets alike.

Let’s look at some key considerations when it comes to implementing a paycheque portfolio approach for retirees and those on the cusp.

Three Key Criteria for Cash Flow (CST)

With a Paycheque Portfolio approach, the focus is on maximizing cash flow, not capital appreciation. We're using the strategy to get the most amount of income for the least amount of volatility, while making sure that those revenue streams are diversified.

However, not all cash flows are created equal. For this reason, investors should consider the following three keys when choosing cash flow-producing assets: consistency, sustainability, and tax-efficiency, or CST for short.

Consistency:

Is the cash flow consistent every month, quarter and year?

Sustainability:

Is the cash flow sustainable for the foreseeable future?

Taxation:

Is the after-tax cash flow relevant?

Consistency is important because it ensures that the frequency of our cash flows matches our needs. By aligning our income stream with our expenses, we make sure we have a solid foundation for our retirement lifestyle.

Sustainability is crucial when we want to ensure that cash flow can be maintained over a long time. By building a diversified portfolio of assets that can withstand market fluctuations, we will ensure that our retirement income remains secure and reliable.

Finally, it's important to consider tax efficiency, as different types of income are taxed at different rates. For example, interest income is often taxed at the highest rates, while capital gains are taxed at a lower rate. By managing our cash flow in a tax-efficient way, we can help keep more of our hard-earned money in our pockets.

Considering the Asset Mix

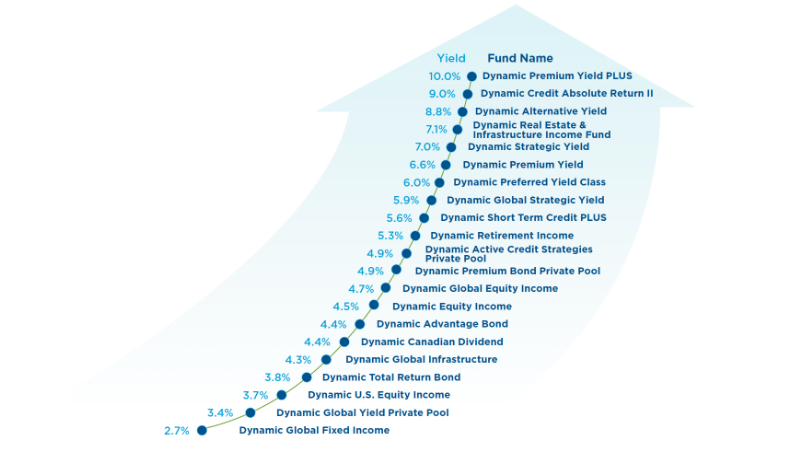

Because the focus is on yield, you’ll see a different asset mix versus traditional retirement portfolios. To successfully implement the Paycheque Portfolio approach, it's important to choose cash flow-producing assets that maximize income and minimize volatility. Here are some traditional income-generating investments to consider when building a Paycheque Portfolio.

Mortgage-backed securities are unique bonds that offer cash flows tied directly to mortgage rates and payments, making them a conservative choice given that investors can potentially benefit when mortgage rates rise.

Issued by companies around the world, global, high-quality corporate bonds offer higher yields than traditional bonds here in Canada. It's a wise decision to focus on the credit-quality space, which can offer attractive yields while maintaining a relatively low potential for default. Dynamic Global Fixed Income Fund provides a unique, actively managed solution to deliver broad access to a wide range of global credit opportunities – much more than just corporate credit and sovereign debt.

Then there's high-yield credit. These bonds can form a steady income stream with yields 3% to 7% higher than traditional government bonds or even GICs (Guaranteed Investment Certificates).

Cash Flow Producing Assets in Retirement

David De Pastena, Vice President of Portfolio Solutions

Additionally, Canadian dividend stocks are an excellent choice for a cash flow portfolio, with low volatility and favorable taxation. With its 20-year track record, Dynamic Equity Income Fund offers a high level of monthly income by investing primarily in high-quality Canadian companies with attractive free cash flows and growth.

There are two other asset classes that retirees should consider when using a paycheque portfolio approach. One of these is preferred shares, which are hybrid investments offering much higher returns than traditional government bonds, but with a favourable tax advantage when distributing dividends. This type of income is taxed at a rate around 30% lower than interest income from bonds or even GICs, making it an excellent way for retirees to earn attractive returns while saving on taxes.

Another asset class to consider is alternatives, which can be used to drive superior yield levels. For example, options income strategies, such as Dynamic Premium Yield Fund, can provide a reliable source of income with an insurance premium potentially in excess of 7% or 8% per year, along with a strong correlation in rising markets.

Built for Income: The Paycheque Portfolio Approach

By building a diversified portfolio of assets that can withstand market fluctuations, we help to ensure that our retirement income remains secure and reliable.

Source: Dynamic Funds, portfolio built using passive ETFs optimized for KYC requirements noted at most advisor dealers

Risk Management: The Golden Window

It's important to remember that there is a specific window of time when risk management is critical. This golden window is usually five years before and five years after retirement commences. Getting clients into this strategy five to seven years before retirement can be extremely helpful, especially in down markets. Clients who don’t need the income will be reinvesting their distributions, which will purchase more units during a downturn and ultimately generate more future income.

It’s also a critical opportunity to help new retirees – before a market correction negatively impacts their account and negatively impact their retirement lifestyle significantly. Failing to act may expose clients to additional risk. That's why that golden window is so critical to focus on. When it comes to retirement planning, it's all about risk management.

Pre-retirement Risk Management

David De Pastena, Vice President of Portfolio Solutions

More Than Just a Strategy

The Paycheque Portfolio approach transcends typical financial strategies. By spending income, not capital, the strategy embodies a commitment to a stable and prosperous retirement, granting retirees the tranquility and security they richly deserve in their golden years.

Email

Email

LinkedIn

LinkedIn

Copy Link

Copy Link