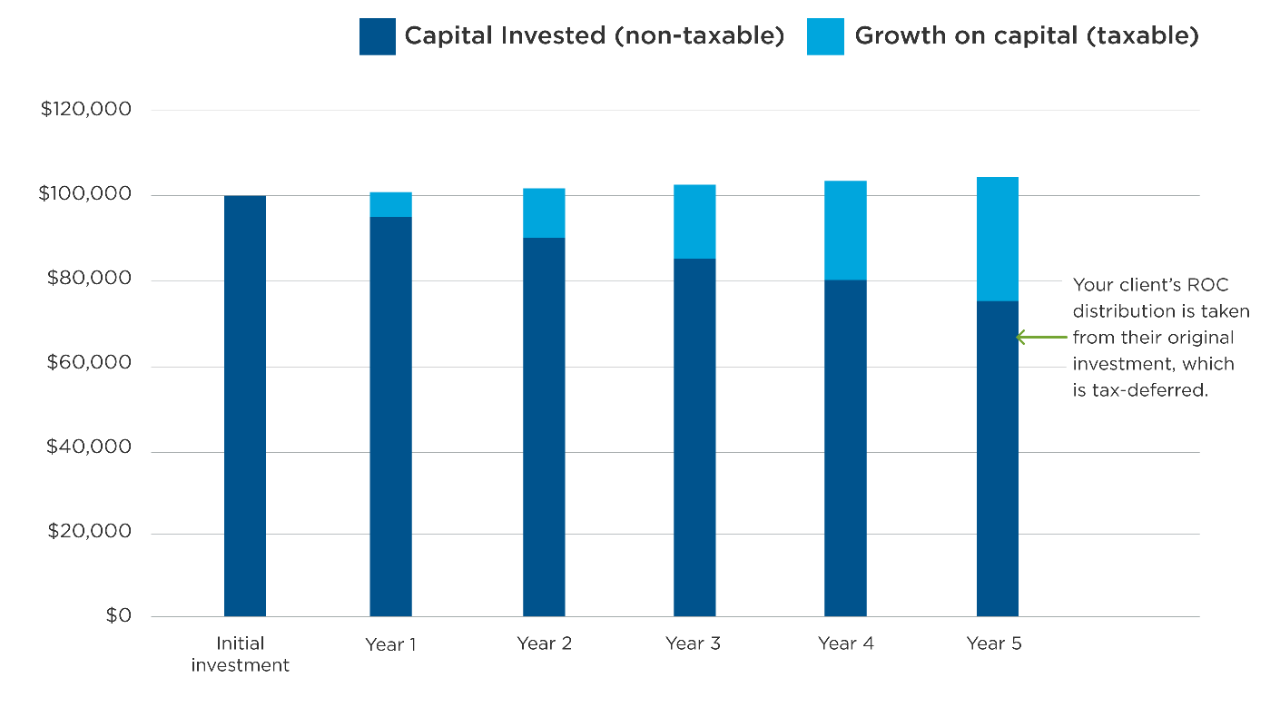

For illustrative purposes only. Assuming 6% rate of return and 5% distribution rate.

Income from an investment in Series T will primarily consist of a return of capital distribution but may also consist of net income and/or net realized capital gains. The return of capital withdrawals will lower the capital of the investment over time. What remains in the account is any growth the investment has achieved over the years on the original investment. Any subsequent withdrawals after the capital reaches $0 are taxable in the form of capital gains, which is currently taxed at a lower rate compared to dividend or interest income.

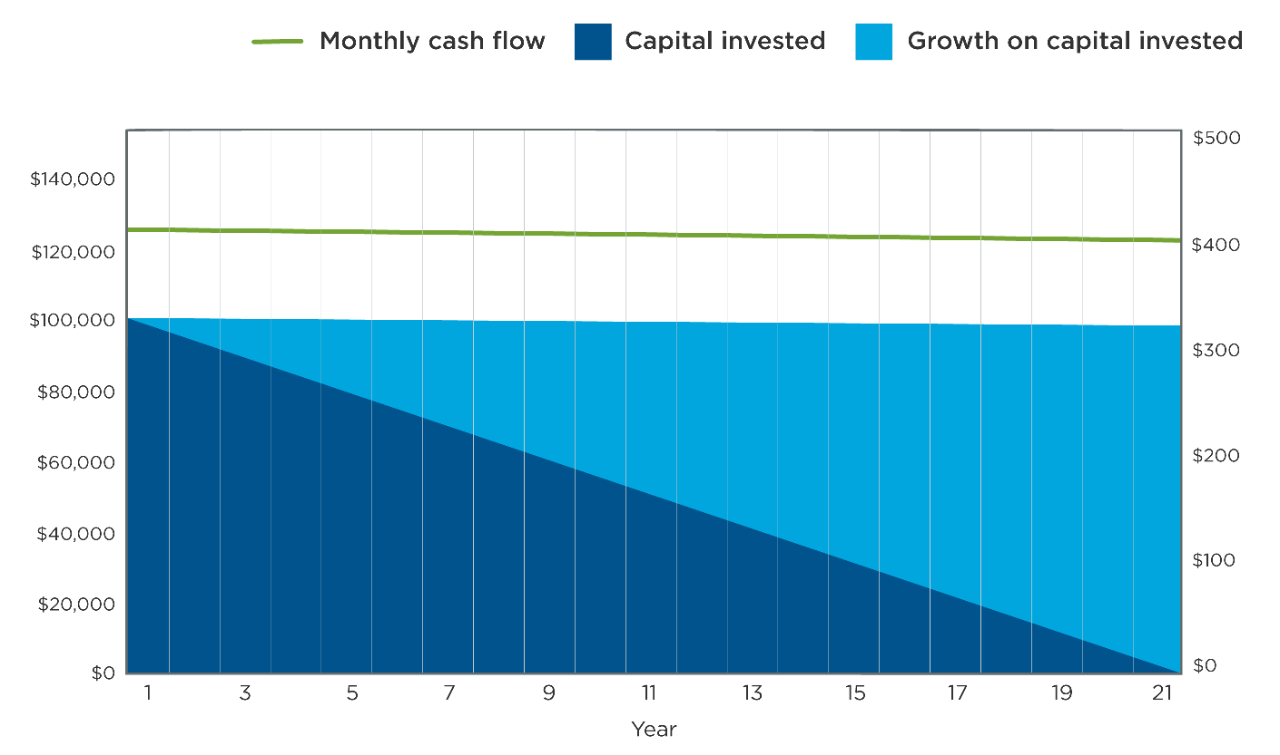

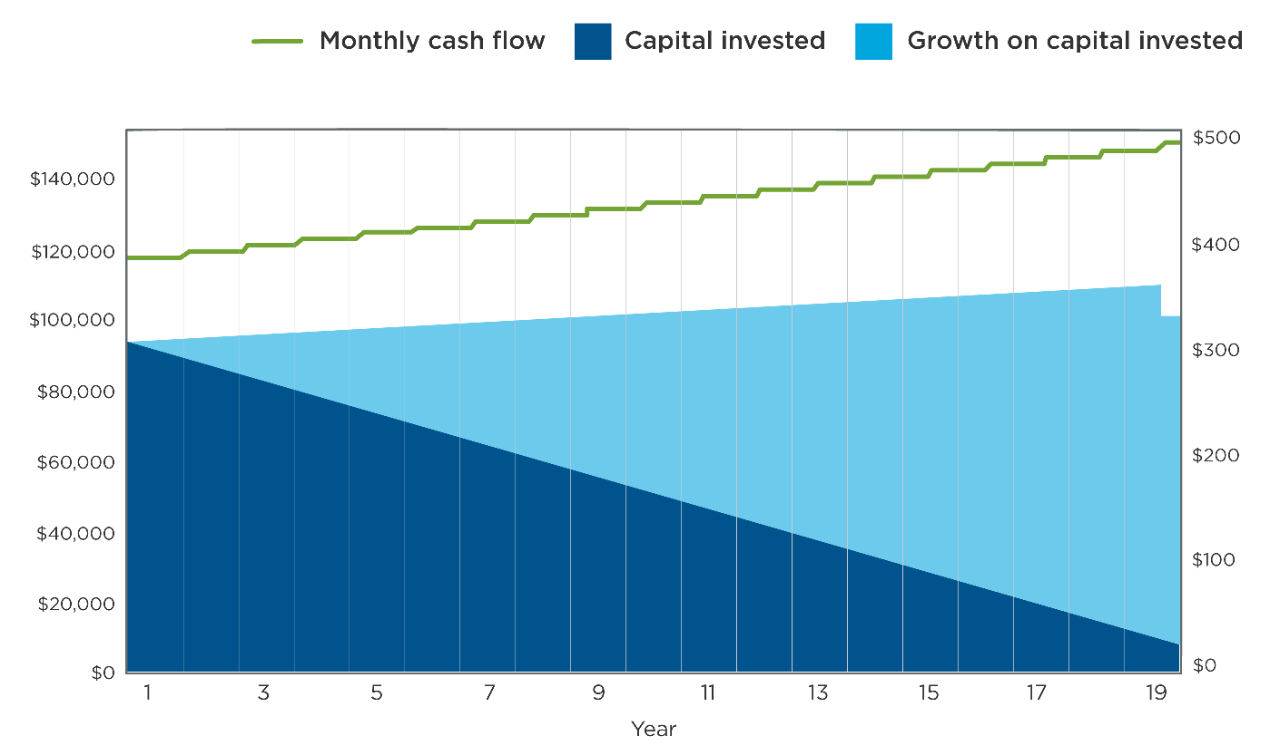

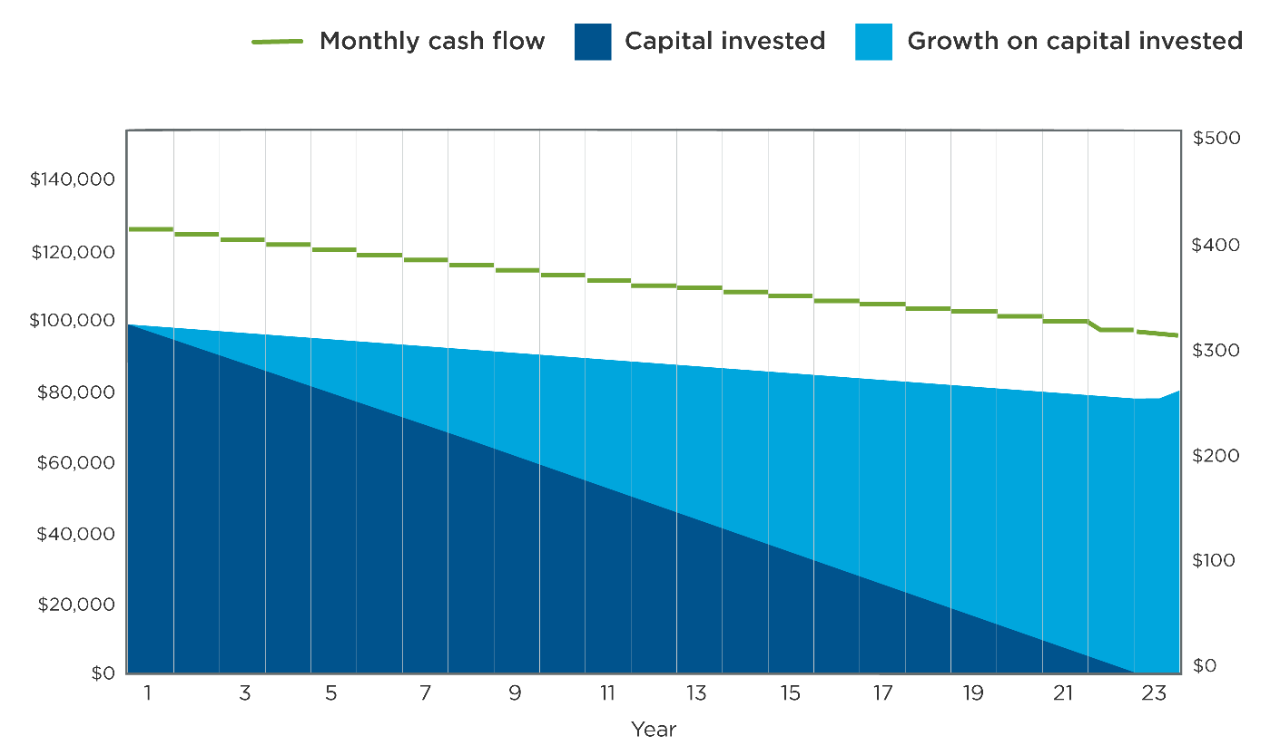

A Series T investment allows your clients to defer the taxes on return of capital distributions they receive, and pay those taxes at a more advantageous time in the future. When your client decides to sell the investment, they will realize a larger capital gain than if they had not received return of capital distributions. However, capital gains are taxed at a lower rate than other income and your client can choose to sell when they may fall into a lower tax bracket, potentially reducing their overall tax bill.

Distributions on Series T may also consist of net income (or dividends in the case of Series T of Dynamic Corporate Class Funds) and/or net realized capital gains.