Given increased market volatility, the impact of inflation and retirees living longer than ever, the dangers of outliving one's assets is a very real concern for many prospective retirees. According to a 2019 report, the Canadian retirement gap – the number of years that seniors might outlive their money – is now 10 years for men and 13 for women. With Baby Boomers retiring in ever-increasing numbers, the coming retirement boom could be a retirement bust if Canadians don’t adjust to the new retirement reality.

Three Key Challenges

The inflation effect

Inflation can erode the purchasing power of money, weigh on bond portfolios and generate headwinds for equity values. With the Consumer price Index hovering near-four-decade highs in both Canada and the U.S., retirees must look to invest in assets that can deliver positive inflation-adjusted returns over time.

Markets are becoming more volatile

From the dot-com bubble to the Great Recession and a global pandemic, markets have seen a number of significant swings over the past few decades. Increased volatility adds uncertainty to one’s retirement plans, and the timing of market drawdowns can severely impact long-term cash flow.

Running out of money

The good news is that Canadians are living longer. However, living longer means that retirees need to accumulate more to fund their desired retirement lifestyle. With retirement periods now stretching more than two decades, the risk of running out of money has become a real concern for many Canadians.

Want to know more?

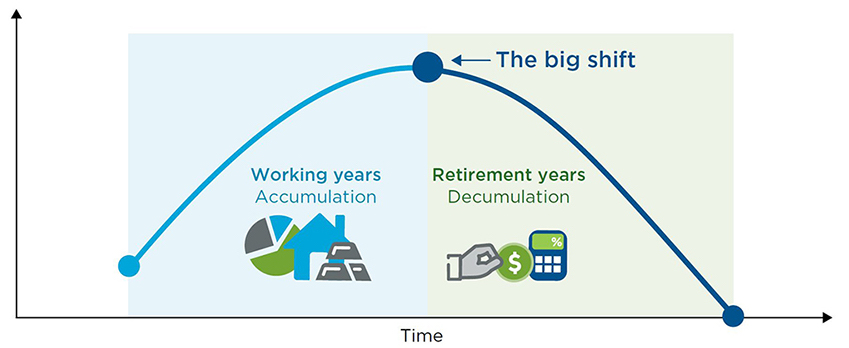

Thriving or Surviving: The Big Shift

At Dynamic Funds, we believe that for Canadians to truly thrive during retirement, their investment mindset must shift upon entering retirement. Instead of using a traditional asset allocation – and systematically withdrawing from those assets during retirement – Dynamic’s Paycheque Portfolio™ approach provides an alternative with potentially less risk.

By prioritizing cash flow-producing assets, retirees can create sustainable cash flow, which enables them to avoid withdrawing assets during market downturns. The result is a "paycheque-like” cash flow stream that pays out regardless of what the market does.

The big shift: From working years to retirement